How to Decide If NOW is the Right Time to Buy a Home

The news media will tell you now is a bad time to buy a home.

Real estate & mortgage professionals will tell you now is a great time to buy a home.

This has been the case for months…years…forever.

Here’s why…

It is in their best interest.

News media likes negative, fear-based stories. Whenever there is bad news, they share it. Rarely do they show feel-good stories. Or news of when things are going normal. They do this because it serves them. It helps them sell advertising. Because…fear sells!

Humans have been conditioned for thousands of years to be afraid of things. It is how we survive. We’ve adapted. Instead of living in caves we live in houses. Instead of being afraid of sabertooth tigers we are now afraid of things that likely wont actually hurt us. It is just how our brains have adapted to survival.

When there is something to be afraid of we pay attention. In terms of the news, this means you watch or read what they have to say. When you stop and pay attention they can get advertisers to pay them to get in front of you. That’s how they benefit by selling fear!

Real estate & mortgage professionals want you to believe that it is always a good time to buy. Because when you sell or buy a home they make money.

When the market is hot you should…buy, buy, buy!! Or sell while you can get top dollar.

When the market is cool you should buy, buy, buy!! Because you can get a better deal.

Who should you believe? How do you decide? How do you know with confidence?

Here is my professional mortgage advice on the matter. I will do my best to remain unbiased with your best interest in mind.

Here is how I see it. I can’t (and probably shouldn’t) sell you through a post on a website. Buying or selling a home is too important of a transaction. You deserve more when making a decision as big as buying or selling a home. And, I don’t believe that a single post would actually be able to sell you on the idea anyway.

I think we are both safe. You can continue reading without worrying about me selling you anything. Just sharing my insight and experience based on 20+ years of getting people into debt…a lot of debt. Here we go…

Overview of what’s covered:

- Fear of a Housing Bubble

- Reality of a Housing Bubble

- Where are Mortgage Rates Headed?

- But, We are in a Recession

- Buy Now or Wait?

Fear of a Housing Bubble

Oh no, the sky is falling. Uh, I mean the bubble is going to POP!

Fear! That’s what this is about. Scaring you.

Check this out…

Diana Olick is a TV news personality who is often featured on housing related news stories. She loves selling fear. Here is what she has had to say over the years:

Wow, right? She has thought the worst of housing for years!

Wow, right? She has thought the worst of housing for years!

Here is what happened over the years as these fear-based claims were being pushed out by CNBC:

- October 2015: “Housing today: A ‘bubble larger than 2006’

- Home prices appreciated 5.1% from $300,000 to $315,000

- $15,000 gain

- August 2016: “We’re in a new housing bubble”

- Home prices appreciated 5.4% from $315,000 to $332,000

- $17,000 gain

- November 2017: “Homeownership doesn’t build wealth, study finds”

- Home prices appreciated 6.1% from $332,000 to $353,000

- $20,000 gain

- September 2018: “It’s better to rent than buy in today’s housing market”

- Home prices appreciated 4.1% from $353,000 to $367,000

- $14,000 gain

- July 2019: “The housing market is about to shift in a bad way for buyers”

- Home prices appreciated 4.0% from $367,000 to $382,000

- $15,000 gain

- December 2019: “Next year will be hard on the housing market, especially in these big cities”

- Home prices appreciated 16% from $382,000 to $443,000

- $61,000 gain

- July 2021: “Housing boom is over as new home sales fall to pandemic low”

- Home prices appreciated 18% from $443,000 to $523,000

- $80,000 gain

That is a total of $222,000 in home value gains that would have been lost!

I don’t know about you, but I am not so sure about the media being the best source for information related to a home purchase (or sale) decision.

The Reality of a Housing Bubble

The media would lead you to believe that we have been in a housing bubble since 2015.

Are we? Is the bubble going to pop? Is this what happened in 2007/2008 when it popped last time?

Let’s look at the facts…

It was Very Easy to Get a Mortgage

The Mortgage Bankers Association monitors how easy it is to get a mortgage. They call it the Mortgage Credit Availability Index (MCAI). The higher the number the easier it is to get a mortgage with a score of 100 being “perfect”.

Here is what it looks like when the bubble popped last time: (we hit a high of about 400 – in other words it was very easy to get a mortgage)

Tons of Homes Were Being Built!

Leading up to the last housing bubble we had four consecutive years of record setting levels of new home construction:

You Had Your Choice of Homes to Buy

The real estate industry tracks a metric called months of inventory. Basically, it calculates how long it would take for all the homes on the market to be sold if buyers bought at the same rate that are in that month.

For example, if there were 100 homes for sale and last month 20 homes were sold it would take 5 months for all 100 homes to be sold. That means there would be 5 months of inventory.

6 months is considered to be a “perfect” or “balanced” market.

In 2007 and 2008 we hit over 9 months of inventory:

Foreclosures Were Out of Control

Foreclosures are a sign that the housing market is in trouble. People can’t afford their homes. No one is willing to buy it from them.

When foreclosures started increasing it was a sign trouble was ahead:

Mortgage Rules are almost “Perfect”

After the housing bubble Federal regulations went in place to monitor and regulate the mortgage industry to avoid what happened in 2008.

There have been a lot of great changes and now mortgage lending rules, according to the MCIA index which monitors how easy it is to get a mortgage is almost “perfect”:

New Construction Homes About Right (probably a little low)

Builders got hurt, big time during the last housing bubble.

To avoid making it worse they just about stopped building. This resulted in 13 years of building below the 50-year average:

Very Few Homes for Sale (but starting to increase)

Home builders haven’t been building which has led to a shortage of homes on the market. But the demand is still there which means the months of inventory has declined since 2018.

There has been a recent increase in inventory levels to 3.3 months according to the National Association of Realtors.

Remember…a “balanced” market is 6 months so we are still very much in a “Seller’s Market” even though it may feel like a bit of a buyer’s market, lately.

No Foreclosures

Ok, so there are some foreclosures occurring. But the number of foreclosures is extremely low.

The Bottom Line: We are NOT in a Housing Bubble

Clearly what we are experiencing now is nothing like what we experienced during the housing bubble in 2008.

Where are Mortgage Rates Headed?

The best way to guess where mortgage rates are headed is to look at what causes mortgage rates to change.

There are two main things to look at:

Treasury Yield

Without going into all the detail about why mortgage rates follow the 10-Year Treasury Yield, just check out this chart:

Clearly, mortgage rates follow the 10-Year Treasury yield.

But there is something else to see here, which you probably didn’t notice. The spread. The difference between the two.

Historically, the spread between the 10-Year Treasury Yield and mortgage rates is about 1.79%. Right now it is about 2.79%!

That means, if we were within the normal spread mortgage rates would be 1% lower than they are right now. It’s likely just a matter of time for that correction to occur.

Inflation

Mortgage rates are also closely tied to inflation as you can see here:

The lines don’t exactly match up like they do with the 10-Year Treasury Yield.

Instead, inflation is a leading indicator of where mortgage rates will go.

Right after inflation goes up so do mortgage rates.

If we can see what inflation is doing we can guess (with some accuracy) where mortgage rates are likely headed. Here is what’s happening with inflation:

Inflation, as of December 2022, actually started to decline on a monthly basis. Inflation is still quite high at 6.5%. Historically inflation has averaged at about 3.8% between 1960 and 2021. This means we still have a lot of improvement to be seen.

The Fed is doing everything they can to bring inflation back down to their target of 2%. They are doing this by “increasing rates”.

The Fed does not control mortgage rates.

The Fed influences short-term lending rates, which impacts the economy, which impacts bonds, which impacts mortgage rates. Mortgage rates and the Fed rate are very different rates and should not be confused.

As the Fed continues to increase rates, slowing the economy and getting inflation under control we can expect mortgage rates to decline. And that’s exactly what is happening:

But, We are in a Recession!

We might be. It’s not official but we have met the criteria for a recession based on how they have defined them in the past.

Being in a recession means it is a bad time to buy…right?

Not exactly. Maybe even the opposite.

If we look back, home prices go up during recessions:

Mortgage rates go down during past recessions:

Of course history doesn’t guarantee anything in the future. There is always the possibility for an exception.

But based on everything else we are seeing it is likely home prices will go up and rates will go down during a recession.

Buy Now or Wait?

I’m a mortgage professional. I make money when people finance home purchases with me.

If you buy a home and need a mortgage I want you to contact me. I am better than most.

- I communicate better

- I take a holistic view when recommending a mortgage solution

- I get creative on finding ways to make the payment as affordable as possible

- I stay engaged for years beyond closing to help you manage your mortgage and overall debt

- I believe in financial freedom so much I wrote a book about it

- I help my clients achieve financial freedom, if they’re interested

Alright, there’s my “sales pitch”. Still with me? Blah, blah, blah, I know. But those things I mentioned above matter. You won’t get that from 99% of the mortgage lenders who want to sell you debt. Find a lender that will find you the best debt and then help you get out of debt and create financial freedom in your life.

Seriously, I am done now. Here is my answer to, “Should I buy now or wait?”

You should buy when it is right for you.

I bought a house in August 2022. I moved from Hawaii to Arizona. It was the right time for me.

Was it perfect market timing? No, but it might have been close. I sold at a good time in Hawaii before the market slowed down. I bought in Arizona before the market made a small correction. If I had waited to buy in Arizona until today I probably could have saved 5% or so on the price of the home I bought.

Do I regret it? Not. At. All.

Here is what I know about real estate…and mortgages.

It is not about timing the market. It is about time in the market.

Home values go up over time. The longer you hold something that appreciates in value the less likely you are to lose money. Despite any market adjustments (a.k.a. drops).

I realize stocks and real estate are very different investments but the idea remains the same. The longer you hold the less likely you are to lose money. Check this out:

- You have a 27% chance* of losing money in the stock market over a one-year time period

- You have a 13% chance* of losing money over a five-year time period

- You have 0% chance* of losing money over a 15-year time period

Source: TD Ameritrade

*Past performance is no guarantee of future results. This is for illustrative purposes only and not indicative of any investment. An investment cannot be made directly in an index. Please go to the source for full details.

Here are the reasons you should buy now:

- You need/want more space

- You need/want less space

- You need/want a different house

- You need/want a newer home

- You need/want to be closer to family or friends

- You need/want to be in a different school district

- You need/want to be closer to work

- You would like to improve your financial position by paying off debt from your home equity

Here are the reasons you should NOT buy now:

- The media tells you that you should

- Real estate agent tells you that you should

- Mortgage professional tells you that you should

- Your uncle tells you he has some inside info and now is the time to buy

- You think rates are too high and you are waiting for them to drop

- You think we are in a housing bubble and you’re waiting for housing prices to plummet

If you want to buy a home read this. If you don’t want to buy a home, move along...

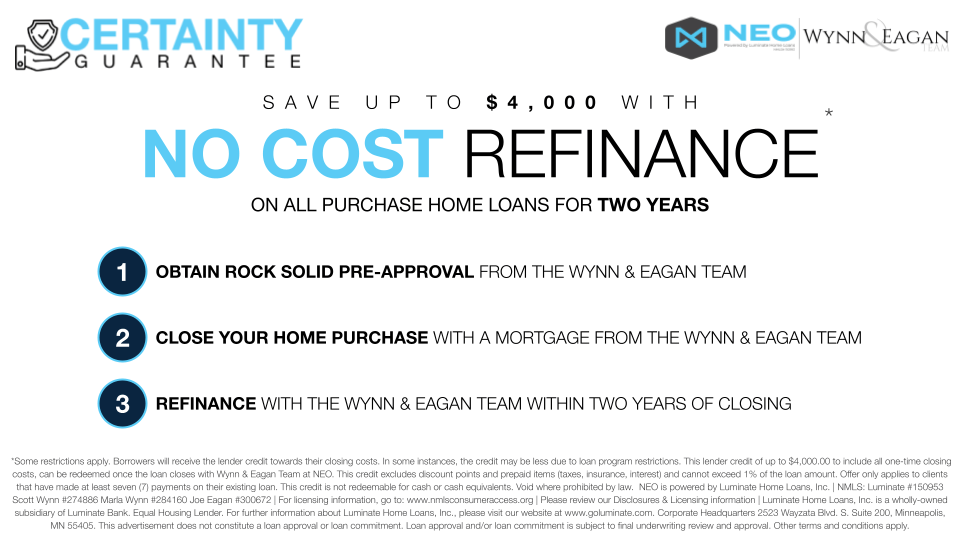

I’d like to give you a bit of peace of mind if now is the right time for you to buy. I want to give you a no regrets guarantee.

I’d like to give you a bit of peace of mind if now is the right time for you to buy. I want to give you a no regrets guarantee.

If you finance your home purchase with me and my team we will provide you with a Certainty Guarantee.

Basically, I don’t want you to try to time the market. It is a bad idea. Even professional forecasters get it wrong…about half the time.

Instead, take me up on this offer. If rates drop anytime within 2 years after you buy a home using us for your mortgage, we will refinance your mortgage at no cost. That way you can secure a home now while home prices are lower than they will likely be in the future. And you get a lower rate if they drop in the next 2 years.

How do you get the guarantee? Our Certainty Consultation, of course. You can schedule a time with our team right here:

Click Here to Schedule Certainty Consultation

The Bottom Line

That was a lot of info. Maybe you just scrolled down here looking for the bottom line. If you did, I would suggest reading through it if you plan to make the decision to buy or sell a home. But, hey it’s your life. You’re the one that has to live with the decision. Not me.

Here’s the snapshot. The juicy stuff. The bottom line.

- The media wants you to be scared so you keep watching the news so they can sell advertising.

- Real estate agents and mortgage professionals want you to buy & sell so they make money.

- Headlines will scare you into thinking it’s always a bad time to buy.

- Data shows that 2022 is nothing like 2007/2008.

- Mortgage rates follow the 10-Year Treasury with a typical spread of 1.79% but we are currently at 2.79% which means rates are likely to come down.

- Inflation is the leading indicator of mortgage rates and inflation is starting to come down giving further reason for rates to drop.

- During recessions home prices normally go up and mortgage rates normally come down.

- Buy when it is right for you!

- When you buy have the peace of mind that if rates drop you can refinance at no cost with our Certainty Guarantee.