Things are finally turning around for the better as far as housing is concerned – and it looks like they might actually stay that way this time!

Mortgage rates have continued to drop over the last couple of weeks, and we are now in the ninth consecutive week of improvement. The average 30-year fixed mortgage rate is now back to where it was in late June!

Existing home sales also increased month-over-month in November, which is great news after five consecutive months of declines. This shows that buyers are becoming more confident in the market and ready to take advantage of improving affordability conditions.

We’re also getting more home supply! Housing starts hit an 18-month high in November and will probably gain even more momentum as we move into 2024, with declining mortgage rates and incentives from builders likely to draw even more potential buyers back into the housing market.

Why Have Rates Fallen So Much?

The decline in mortgage rates happened after continued news of easing inflation and as the Federal Reserve decided to keep the Fed Funds rate unchanged while hinting at possible rate cuts in 2024.

With the inflation rate hitting the 2% target and unemployment still relatively low, the Fed voted unanimously during their December 13th meeting to keep the Fed Funds rate steady between 5.25%-5.5%. They also mentioned they expect at least three rate cuts in 2024 if things continue to improve.

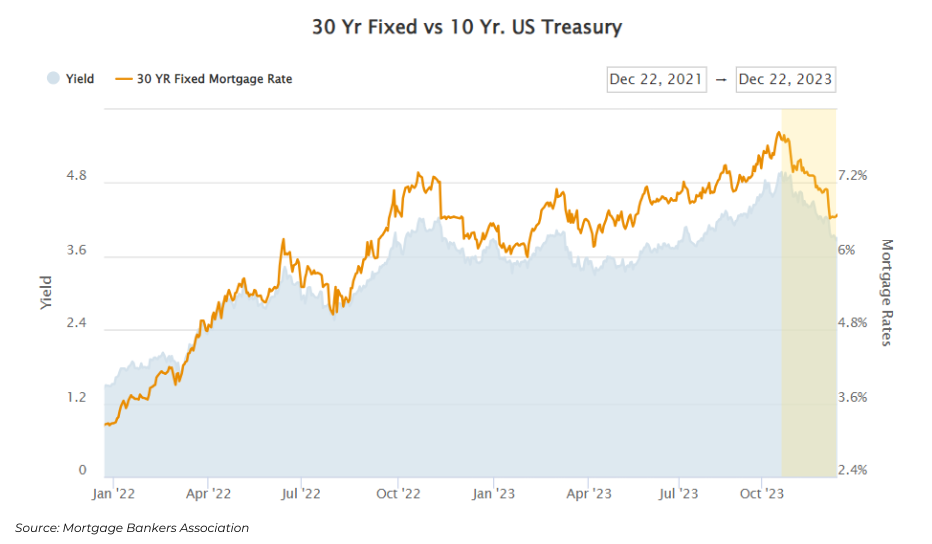

Mortgage rates don’t exactly follow the Fed Funds rate, but instead track the yield on the 10-year U.S. Treasury. The yield has been falling since mid-October and saw a big drop immediately following the Fed’s comments.

Mortgage Application Volume Increasing

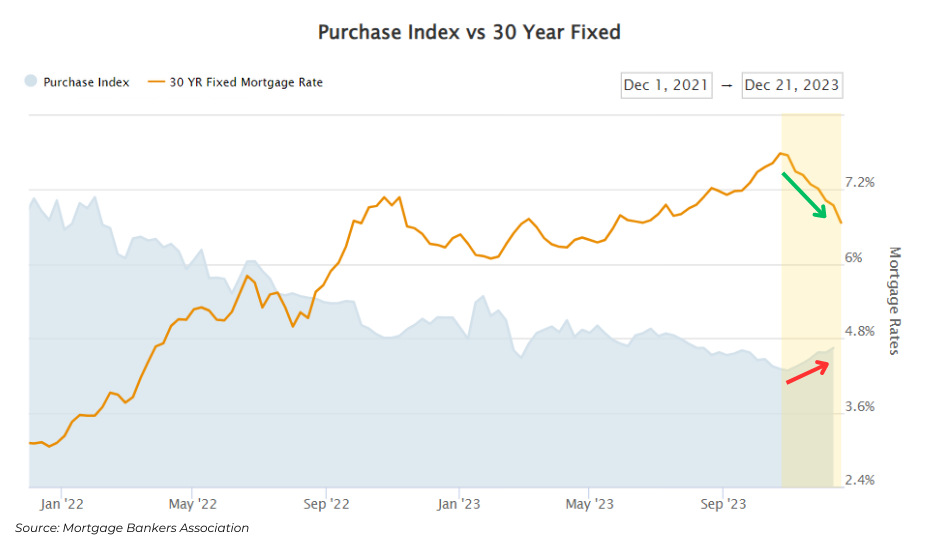

After mortgage rates saw a large decline in mid-November, both purchase and refinance applications increased to their highest weekly pace in five weeks.

The chart below compares mortgage application activity (the MBA Purchase Index) and movement in the average 30-year fixed mortgage rate. The Purchase Index includes all mortgages applications for the purchase of a single-family home. It covers the entire market, both conventional and government loans, and all products. The Purchase Index has proven to be a reliable indicator of impending home sales. (investing.com)

As you can see, even a small drop in rates results in a LOT of demand for mortgages, which never happens this time of year. When rates fell in November, we saw application numbers like we saw in July and August at the peak of the homebuying season.

Most of this purchase activity has been for new homes. According to the MBA data, new home purchase mortgage applications soared by 21.8% in November compared to a year ago.

Home Inventory and Sales Also Rising

Lower rates are bringing some buyers off the sidelines and increasing demand, but we still have a long way to go as far as home supply is concerned. There are still limited options on the market as the many homeowners who locked in ultra-low mortgage rates in recent years remain reluctant to sell. This is what’s keeping housing inventory at historical lows.

Luckily, we’re starting to see some improvement on the inventory front. A surge in construction and more existing homes coming on the market should give buyers more opportunities in the new year.

Housing starts jumped in November and passed 1.5 million units for the first time in 2023. The U.S. Census Bureau and the Department of Housing and Urban Development said construction began during the month at a seasonally adjusted annual rate of 1.560 million residential units – increase of 14.8% from October’s rate of 1.359 million units.

Existing-home sales also showed gains last month, breaking a streak of five consecutive monthly declines. The National Association of REALTORS® recently reported that existing-home sales rose 0.8% in November. NAR is confident that figure will grow even more in the coming months as borrowing costs fall.

What Does This Mean for You?

We are on the right track to lower mortgage rates that finally stick!

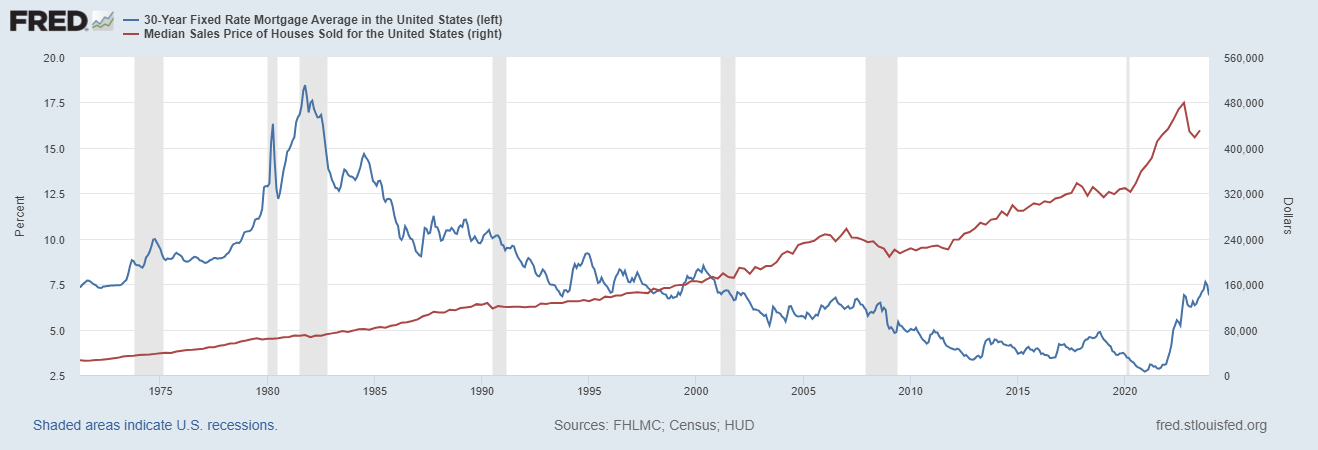

There is a common misconception that the only way for housing to become more affordable is for the market to “crash” and bring home prices down by double-digit percentages.

Supply and demand tell us that this will not happen, but the recent drop in mortgage rates and subsequent surge in buyer demand do tell us that when affordability improves, more people will come off the sidelines.

Historically, high mortgage rates have never been a catalyst for a housing crash. As you can see in the chart below, over the last 50+ years it was quite rare for mortgage rates (blue line) to rise while home prices (red line) simultaneously dropped. This only occurred in the early stages of the Global Financial Crisis and during the recovery.

We are optimistic that 2024 will continue to bring lower mortgage rates and provide some relief for homebuyers.

This won’t be an immediate drop to 5% mortgage rates. We will likely see some ups and downs in the months ahead, but the recent economic reports are clear indicators that the trend has reversed from higher and higher mortgage rates to improving affordability ahead.